The COVID-19 pandemic has changed many priorities and created a new reality in its wake, but it hasn’t altered the need to deploy smart outsourcing strategies. If anything, the past 12 months have underscored how critical it is for companies to effectively manage IT, service providers—those that offer digital capabilities and business process services—in order to survive a crisis and, at the same time, transform to lead in the aftermath.

Moreover, the crisis has reinforced companies’ symbiotic relationships with their service providers. That’s evident from a survey that BCG conducted in the last quarter of 2020. We found that companies will continue to depend on service providers even though they will also invest more in developing in-house capabilities.

The results also reflect the state of companies’ digital transformations. Contrary to the popular notion that businesses sustained all their digital transformation projects last year, the survey shows that many companies were selective about which ones they pursued. And while 76% of respondents expect to slow down some transformation initiatives during the next 24 months, 96% expect to accelerate the execution of some transformation projects.

In this article, we shine a light on these findings and their implications for the future.

COUNTING ON SERVICE PROVIDERS TO NAVIGATE THE CRISIS

All through 2020, as the pandemic raged and governments around the world were forced to impose, and then reimpose national lockdowns, the world’s economies were paralyzed. To understand the impact of the COVID-19 crisis on outsourcing, BCG conducted a survey of 200 global companies with large IT and business-process outsourcing footprints. (See “About the Survey.”) We found that 82% of the respondents saw revenues fall, 78% faced operational challenges, and 68% had to cope with service provider-related challenges.

Finding it difficult to manage these forced digital transitions on the fly, many companies turned to their service providers for support then and have been expanding their relationships with them. “We are deepening our relationships with the [service providers] that saw us through [the initial crisis],” said a CIO of a global mining company. “They’ve been supportive and particularly good. We haven’t had a major incident throughout this period.”

Many companies that turned to their service providers for support are expanding their relationships with them.

Some companies were able to cope with the crisis because of the portfolio sourcing strategies that they had adopted before the pandemic. (See Exhibit 1.) They had been distributing the services they need to offshore and onshore providers, as well as investing in building in-house capabilities. In fact, 67% focused on developing in-house capabilities, and 66% concentrated on increasing insourcing levels. These companies tasted relatively more success during the crisis than other respondents.

While many companies rely on a global footprint of service providers to prevent service breakdowns, that model doesn’t factor in the possibility of a pandemic washing over the world. Service providers, particularly in outsourcing hubs such as India and the Philippines, were hit hard, although they did their best to cope. For example, a service provider in India rented an entire hotel to ensure that its employees could work in a bubble. The company provided accommodations, access to food 24-7, stable broadband connections, and, later, regular COVID-19 testing. Other service providers negotiated with local governments to ensure that power cuts to their employees’ homes-turned-offices would be limited or, at least, predictable.

PUSHING AHEAD, CAUTIOUSLY, WITH A TRANSFORMATION

Businesses didn’t allow the urgent to drive out the important, though. Sixty-one percent of the companies we surveyed said that they accelerated parts of their digital transformation over the course of the year, although 42% noted that they slowed down some projects. (See Exhibit 2.) Thus, the popular perception that digital transformation has only accelerated in 2020 may be misleading, with some qualifications becoming necessary to understand the ground realities.

Importantly, most enterprises plan to persist with their digital transformation agenda; in fact, 96% of the companies we surveyed expect to accelerate the execution of their transformation-related projects over the next 24 months. These companies anticipate their immediate focus to be reinforcing the IT function, with more investments in cybersecurity (55%), given that people will continue to work from home; automation (49%); cloud migration to reduce costs (47%); artificial intelligence (AI), machine learning (ML), and analytics (46%); and crowdsourced innovation (35%). That focus is consistent with their pre-pandemic agendas: 80% had been concentrating on cybersecurity, 76% had been prioritizing moving to the cloud, and 72% had been focusing on deploying AI, ML, and analytics well before the crisis.

However, other companies will be selective about the digital transformation projects in which they will invest in the near term. Of the 76% of companies that expect to slow some of their transformation projects, 25% are likely to reduce their investments mainly in risk management, 23% in supply chain management, and 22% in HR processes. The main reasons that these companies offered for reducing these investments in the short run were either the lack of financial resources or a reprioritization of strategic objectives (74% of respondents in both cases). As a global fashion retailer succinctly put it: “We pushed ahead with all the initiatives that related to our customers and their digital journeys but paused almost anything that wasn’t connected to our digital transformation.”

Interestingly, companies whose service providers were affected by the crisis were more likely to slow down transformation projects. “One high-profile project stalled because we needed to fly in people from India to do the work, and we couldn’t get them in [because of the COVID-19 crisis],” explained a CIO of a global minerals company. “We had to stop for six weeks, regroup, and think about how best the work could get done [under those circumstances].”

Companies that are planning to accelerate transformation projects anticipate relying on service providers more heavily.

REVAMPING SERVICE PROVIDER STRATEGIES

With the pandemic likely to persist well into 2021 despite the recent launch of coronavirus vaccines, businesses are realizing the necessity to revamp their sourcing strategies. Building on the past year’s responses, companies are adapting their outsourcing strategies to get a bigger bang for the buck.

Before the pandemic struck, 46% of companies’ budgets were spent onshore, 23% was spent nearshore, and 31% was spent offshore. Most companies will persist with a similar mix over the next 24 months, our data shows. If the proportion of companies’ budget allocations changes, 61% of respondents said that the driver will be the need to reduce costs because the global economy isn’t recovering quickly enough, while 53% said that it will be the result of companies taking steps to ensure business continuity should more disruption occur due to a surge in the number of coronavirus cases.

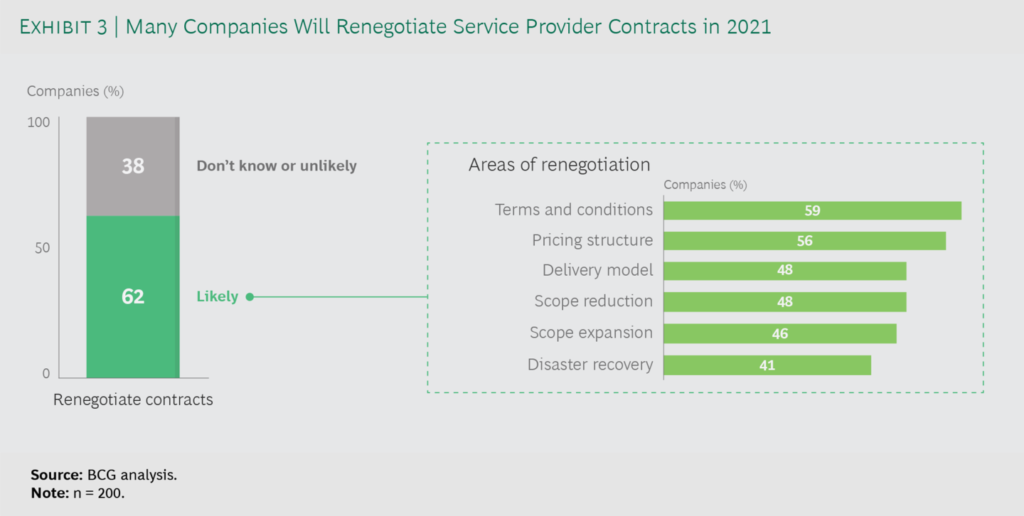

Out of an abundance of caution, many companies—62% of our sample—are very likely to renegotiate outsourcing contracts. (See Exhibit 3.) The areas for future discussion will likely be changes in the contractual terms and conditions, pricing structure, delivery model, and scope of providers’ services. At the same time, companies said that they are looking to service providers to shoulder more risk, particularly when it comes to maintaining the continuity of business operations.

Many companies appear keen to build capabilities in-house to mitigate the risk of a transformation failing should gaps appear in service providers’ capabilities or performance. Attracting talent is the stiffest hurdle, though. Eighty-nine percent of the companies we surveyed reported that access to digital talent is one of the biggest challenges that they will face in the next two years. Correspondingly, an almost equal proportion of companies anticipate greater dependence on IT service providers in the same period. That’s particularly true of companies accelerating or rethinking transformation agendas.

To mitigate the risk of a transformation failing, many companies appear keen to build capabilities in-house.

Companies usually spend most of their outsourcing budgets on critical areas, but they may be more comfortable onshoring, rather than offshoring or investing in in-house capabilities in the future. Forty-six percent of respondents said that they would invest more in developing in-house capabilities, suggesting that onshoring will continue to play a key role. Explained the CIO for a large mining company, “We offshored a lot, but we want to keep the deep thinking around our pain points onshore. We like to work with good service providers that know our back-end systems well. That way, whenever necessary, they can step in and help our solutions teams, too.”

Only companies whose revenues declined in 2020 are trying to save costs by reducing their onshore footprints and shifting to nearshoring and offshoring. Many of the companies that we surveyed expect to increase their investments in delivery centers that focus on specialized areas such as software architecture and engineering (51%), application development (59%), application maintenance (55%), testing (53%), product design (52%), and business processes (52%). However, 11% are planning to reduce their investments in delivery centers, with 6% thinking about divestments. That’s a refreshing contrast to 2008, when, in the aftermath of the Great Recession, several companies—including AXA, Aviva, Citibank, Fidelity Group, Prudential PLC, and Philips—auctioned off delivery centers to generate much-needed liquidity.

RESHAPING THE FUTURE OF OUTSOURCING

In 2021, almost half of all the companies we surveyed will outsource more work than they will do internally. That leads us to the question: Although the future has never looked less clear, what are the key implications of our survey for businesses’ sourcing strategies? Companies should manage their outsourcing strategies in the future by taking five steps:

- Focus on resilience. Companies must ensure that staying in business and bouncing back from adversity are two key considerations when refining IT sourcing strategies. Businesses have to incorporate new ways of working—particularly working from home, which is becoming a standard operating procedure—into their future plans. Don’t forget, surveys show that as many as one-third of employees worldwide are unlikely to enter an office again.

- Be selective about partnerships. Businesses must become more strategic about their choice of service providers. Our survey shows that companies work with as many as five service providers, on average, but developing deeper relationships with fewer partners may be the way to go. That will help create ecosystems of digital innovation for many companies.

- Future-proof contracts. Companies will have to change the nature of contracts so that they share more risks and rewards with service providers. Our survey shows that executives expect a rise in the use of outcome-based contracts (47%) and joint ventures (47%).

- Persist with the transformation agenda. Companies must push ahead with digital transformation projects, although they may do so in a nuanced fashion. After identifying nascent hardware and software trends—such as cloud-native architectures, highly distributed applications, and the need to support many different kinds of interfaces such as voice, wearables, touch, augmented reality, and virtual reality—leaders must pick and choose their transformation thrusts over the next 12 to 24 months. That will enable them to figure out the best way to plug capability gaps and determine the kinds of service providers they will need in order to do so.

- Bridge talent gaps. Every enterprise must re-evaluate the capabilities that it can develop in-house with the talent it has and determine which ones to procure from service providers. By building capabilities in-house, companies can reduce the risk of their transformation projects stalling and turn to service providers in areas where they suffer from talent gaps. In fact, some companies are trying to develop capabilities in tandem with service providers—a trend that is likely to grow in the years to come.